The COVID-19 pandemic has wreaked havoc across the world, not only with its sheer magnitude of suffering and loss, but also has successfully managed to bring otherwise resilient economies to a grinding halt. This has had widespread ramifications on the workforce in general, and has been amply magnified for the neglected strata of the society. The CMIE’s estimates on unemployment shot up from 8.4% in mid-March to a whopping 23.4% in the present day. Thus, ameliorative steps, both fiscal and monetary in nature, are the need of the hour.

At this critical juncture, it is essentially a gamble on predictions and forecast. But to sit idle is not an option at all. Fiscal policies are clearly more effective in dealing with a pandemic situation. On the fiscal front, the government has a smorgasbord of options available on its platter. Most advanced economies have adopted a relief package worth 10% of their GDP. In contrast, the GoI has drawn up a plan that expends ₹2 lakh crores for immediate relief only, estimated at 1% of the GDP. An urgent need is to increase the transferred sum to a more sustainable figure, around ₹7000-8000. This may have the effect of inflating the fiscal deficit, but a deficit should be the least of worries in times of crises. KPMG’s report on the impact of COVID-19 in India suggests consumption figures will be the worst hit. Hence, an effort may be made to reduce the personal income tax rates for the time being, so that people have money in their hands to spend on once the situation improves. This will also have a stimulating effect on the economy, by creating a demand surge. The Centre can also further slash the corporate tax, thus aligning it with the East Asian models, which will propel a tendency to invest on part of the corporates. Further, the government can also extend the deposit date for advance tax by a period of six months, which will help crucial sectors as MSMEs to deal with reduced operating margins.

Inflationary worries, particularly on foodgrains, can be curbed by utilising the surplus stockpile available with the FCI. Naturally, greater supply of basic food items through the PDS system, therefore, should also be a focal point. A massive prop in healthcare allocation is also necessary on an immediate front. The Centre’s own National Healthcare Policy envisages a spending of 2.5% of the GDP on health infrastructure, but the present allocation of around 1% of the GDP considerably languishes behind the objective. The Centre now has the added responsibilty of identifying critical sectors, such as auto, pharma and telecom with reliance on global supply chains, and work strategically to bring down foreign dependence by building alternative options. An extension on payment of AGR dues by the government may also be filed for the consideration of the Supreme Court, to assuage the telecom industry’s valid concerns for the time being.

On the monetary front, the RBI’s intervention to dramatically slash rates by 75 bps will have a positive effect on credit availability in the market. However, it is to be noted that monetary policy will have a very little impact on anchoring the economy. While a monetary policy is hugely influential in addressing demand shocks, it appears quite blunt while dealing with supply-side shocks. Thus, a rate cut can have at best a transient effect on market sentiments, but guarantee nothing in permanence. Not all is lost, however: a three month moratorium period extended by the RBI to all EMI debtors will have a beneficial impact on driving consumption higher. Similarly, a slash in CRR requirements and reverse repo rates will ensure that banks have more money to lend with them, and ensure that expansionary tendencies are not curtailed due to a lack of credit.

The COVID-19 crisis brings with it an opportunity to reflect and bring about structural changes in the economy. It solidifies the belief that dependence on China as the global manufacturing hub can no longer be relief upon. Resilience from external supply shocks can only be compensated if localisation of key sectors is worked upon. The lockdown has also brought about a massive adoption of digital technologies, which is a welcome development. Furtherance of Digital India-centric policy can help aid recuperating businesses and industries. It has also proven how important it remains for the corporate to be financially prudent and conserve cash – as a buffer measure- to effectively steer itself out of unpredictable times as these. India can present itself as a viable alternative for the hub of global manufacturing. Can our policies step upto it?

The coronavirus threat has led most nations to take preemptive measures and isolate themselves from the world at large. While lockdowns and cordoning off places have become the norm, the economic tradeoff- that of the cost to the national economy in exchange for “flattening the curve”- is humongous. While India and the world grapple with an exponential progression in the number of COVID-19 cases, we could perhaps take a leaf out of the book of South Korea and China, both of whom have had incredible success in containing the virus within manageable proportions.

India’s draconian lockdown, for twenty-one days and extending to all citizens barring the essential services, is a move inspired by China’s dramatic lockdown of the industrial town on Wuhan- widely considered as the epicentre of the crisis. The lockdown on Wuhan and other provinces in the vicinity ensured that the virus could not spread beyond marked geographical areas. From there on, China flexed its monetary muscle and manpower to construct dedicated hospitals in record time, provide relief materials to all affected residents, and ensuring strict compliance with the defined laws. While India has been able to replicate the imposition of a national lockdown, it is clearly found lagging in other sectors. It did not take into account the spiralling discomfort of the informal sector- which employs 94% of the workforce and accounts for 45% of the national output. The Chinese response to the pandemic in economic terms was to unleash a $394 billion-dollar (2.77% of GDP) stimulus package for reviving domestic growth affected by the outbreak. India has announced a measly $22.5b revival plan – worth approximately 0.77% of India’s GDP. Furthermore, while China has 4.3 beds per 1000 people, India has much less, approximately a 1:1000 ratio when it comes to bed availability.

Perhaps the wiser route could have been finding the middle ground between the Chinese version of lockdown and South Korea’s rapid test-and-treat model. By avoiding closure of industries, Seoul managed to escape the economic cost of flattening the curve- as described in the introduction- and it did a pretty good job at that. Its highly disciplined workforce, led by a proactive government had embarked upon the model of high testing rates to detect and isolate all affected individuals. It is an important lesson for India to partake. Transparency in data, especially in challenging times as these, is essential to making a quick recovery. Any delay in data coordination or a deliberate attempt to veil the actual number of cases may prove to be costly as time advances. States like West Bengal share data once every three days, thereby hampering smooth coordination. Further, the Central government should step in and mandatorily fix a testing rate per million of the population; varying testing rates across states will bring with it varied success outcomes. While South Korea had a testing rate of around nine thousand per million, India’s figures reflect poorly at only ninety-three per million. By opting for a complete lockdown, India also has inflicted upon itself a great economic cost which it has to bear once the crisis resides.

Early action was another boat that the Indian government failed to hop onto. The South Korean government was instrumental in detecting the early cases, and immediately got in contact with pharmaceutical companies and asked them to ramp up production of testing kits. Today, South Korea produces around 100,000 kits per day- and now is in talks with other countries to export it. India had maintained a lackadaisical attitude in the initial stages – with religious congregations and expos in full swing – until it occurred to administrators that it was time to take action. Thus, it missed the boat to ensure a quick solution to the puzzle at hand. South Korea also immensely benefited from enlisting the help of the citizens to ward off the threat as a collective society. Due credits should be accorded to India in this regard. The government was prudent to create and distribute an app, called ‘Aarogya Setu’, which relies on self-declaration and via GPS technology, makes aware a person who has crossed paths with a potential victim of coronavirus.

Yet, positive mends are being made. Several politicians have stepped beyond their party lines to tackle the pandemic. Shashi Tharoor spent his MPLAD fund to procure 1000 rapid-testing kits for use in his constituency and beyond. The Odisha government, under Naveen Patnaik, was instrumental in getting mining giants to spend on dedicated COVID-19 hospitals with a combined capacity of a thousand beds. Perhaps the most commendable of all is the Delhi government’s, led by Arvind Kejriwal, model of ‘5T’- which encompasses testing, tracing, treatment, teamwork and tracking and monitoring. It is in the interest of the people at large that after several years of neglect and ignored recommendations of a large number of specialised committees, the government acts of its own accord and prepares to strengthen the health infrastructure in India now. But mindless spending will not help the process. It should also be followed up with the establishment of high-quality, government sponsored medical institutions and colleges that seek to promote a research-oriented approach to learning, rather than the conventional syllabi over the decades. Such training will also help bridge the discord between a large number of hospitals being set up and the stark deficiency of doctors on duty. It is time the government does its bit to thank the countless health workers putting their lives at stake- not by instances of moral support alone- but by fundamentally bettering the faltering public health system in India.

The Finance Minister’s ₹1.7 lakh crore stimulus package, to help India tide through the harrowing times that the coronavirus lockdown presents, is a welcome move. Barclays pegs the economic cost of the 21-day lockdown at ₹9 lakh crores, or around 4% of the Indian GDP. The biggest highlights are that of medical coverage for the health workers, to the tune of ₹50 lakhs, and extended rations for the poor (10 kg rice/wheat, and 1 kg of pulses for the next 3 months) along with Direct Bank Transfers (DBTs) for the needy.

FM Nirmala Sitharaman, while addressing the press

The government has also systematically allocated resources so as to ensure smooth implementation. The Ujjwala scheme will provide 8.3 crore BPL families with free cylinders for the next three months. The daily wage rate for MNREGS workers has been hiked by ₹20 to ₹202. The old, infirm and widows will be paid an ex-gratia amount of ₹1000, which will be paid in 2 installments. Additionally, 20 crore women with Jan Dhan Yojana accounts will also be entitled to ₹500 per month, for the duration of the next three months to compensate for the downturn during the lockdown phase. For the organised sector, Sitharaman said EPF contribution of both employer and employee (12 percent each) would be paid by the government for the next three months, with some riders on the inclusivity net of such firms.

However, it is to be noted that the cash transfers along with the MNREGS hike is very minimal, and may not bring substantial relief. The MNREGS hike was due anyway. However, as many states have closed down the sites for such labour work, it is unclear how many can pragmatically benefit from such an increase. The relief package comes ladled with considerable financial burden for the government, at a time it grapples with the slowdown in the domestic economy and a low-lying world order. As the heavy bill of ₹1.7 lakh crores cannot be raised by taxation alone, the government may eye raiding the RBI’s treasure trove in the form of annual dividends, and possibly look for deficit financing through bonds.

The relief package comes with a considerable financial burden for the government, at a time it grapples with the slowdown in the domestic economy and a low-lying world order. However, in coming out with such a package, the government has done the right thing on both the personal and the societal level. It has avoided unwarranted deaths out of starvation, neglect, and other tragedies, while at the same time, it has also ensured that small industries and firms are not obliterated by the crisis that has the potential to set the economy into an anarchical state. The markets, which rallied by several points today, is perhaps indicative of the same. Yet, immediately after the crisis resides, the government must take immediate steps to kickstart the faltering economy, failing which the benefits provided for by the stimulus package would be foiled.

It would only be a matter of time before we can academically evaluate the benefits of government intervention into the humanitarian challenge that confronts India uniquely.

An unilateral thrust on the growth perspective (based on GDP figures alone) being central to the measure of human progress had led to a severely skewed society by the end of the 1980s. This was a phase where rapid de-industrialisation was met with hurried globalisation in the West; firms were growing ever larger; and markets were precipitously moving towards monopolistic tendencies. Economic disparities between the rich and the poor richocheted; and it was evidently clear that the ‘real wealth’ of a nation lay not in its present ascendancy, but in the development and building of the ‘human capital’, or intellectual resources. Amartya Sen, recipient of the 1998 Nobel Prize in Economic Sciences, was rewarded for having pioneered the concept of the Human Development Index. What was so very remarkable about Sen’s work then, that changed the worldview on the idea of human development and societal progress by panoramic proportions?

A LOOK AT THE INDICES

The answer to the question requires a multi-pronged analysis into the factors that determine mankind’s advancement over a period of time. The Human Development Index (HDI), a score between 0 and 1, looks into the input variables of life expectancy, education and standard of living as determinants of the HDI score. A higher HDI index is reflective of a country that is substantially ‘developed’, in other words, a nation with a HDI score 1 indicates a highly sophisticated society that has a reasonably high average lifespan, good education standards and a fairly decent standard of living. The arrival of the HDI as a parameter helped governments around the world to engineer a transition from a singular focus on GDP-oriented growth policies earlier to the brand of welfare economics. The UNDP’s HDI Report 2018 ranks India with a score of 0.64 at the 130th position, which classifies it as ‘medium human development’.

HDI sensitised nations about the diminishing importance of income alone to adjudge the progress made by a country, yet, it was not enough to provide an exact idea of the scale of deprivation faced by the population. While most countries maintained some form of a record of poverty levels, these statistics did not signify much other than an income handicap. In 2010, the United Nations Development Programme (UNDP) collaborated with the Oxford Poverty and Human Development Initiative (OPHI) to launch the Multidimensional Poverty Index (MPI)- a three dimensional overview into various factors resulting in true poverty. The MPI scale focuses on establishing trends of quantifiable deprivation amongst people across the world. The MPI also uses in broad sense, the same set of parameters that goes for calculating the HDI score- but it is more exhaustive in nature. While HDI calculation involves a single indicator for each dimension, the MPI calculation deals with respecting data from multiple sources from each applicable dimension. This is one cause for the MPI index being available for just over 100 countries, while the HDI index is almost accessible for every country today. While both the HDI and the MPI serve as fantastic indicators for societal development, critics have often slammed the indices for not taking into account the “moral, emotional, and spiritual” dimensions of poverty. The Global Happiness Index, conceptualised of late, is an attempt to correct that anomaly.

The World Bank in 2018 released a new report, titled the ‘Human Capital Index’. It expands on the idea that for sustainable long run growth in the future, nations must ensure considerable funds for the advancement in sciences and technology. Paul Romer, who shared the 2018 Nobel Prize in Economics, based his theory on economic growth with ‘endogenous technological change’- more is the number of people working in the knowledge sector, greater is the probability that the country is on the road towards prosperity. Incentivization of innovation, along with a increase in public spending on higher education and healthcare results in a workforce that is not only skilled, but also maintains higher productivity over the long run due to access to better healthcare facilities. In the inaugural report launched by the World Bank, India is ranked at the 115th position out of a total of 159 countries that were evaluated.

THE WAY FORWARD

The triad of development indices, namely the HDI, MPI and the HCI, have enabled policymakers to frame legislation that can over time, change the dynamics of an economy. These parameters are also a great aid for a nation to align itself with the UNDP’s Sustainable Development Goals (SDG). India, despite having the advantage of its demographic dividend (average age in India is only 29, with 65% below the age of 35), has mostly been ranked lowly in all the three indices. India’s mediocre performance on the rankings may look astonishing on first glance, but it is not impossible to dissect why. A nation teeming with almost 1.3 billion people will have a natural strain on its resources. The 2018 Oxfam report also brought to light how India’s top 1% possessed 73% of the national wealth- while the basal rung saw their fortunes rise by only 1% for the same year. In his book ‘People, Power and Profits’, Joseph Stiglitz argues that a person born under the curse of poverty has a very low prospect of escaping the poverty trap- indicative of the dampening consequences of widening inequality. The same is true for India. Rise of inequality, coupled with poor grassroot-level implementation of developmental programmes, have reared their ugly head as a draconian duo- a true malaise for an otherwise aspirational population.

The glaring fault-line lies in the fact that despite heavy investments being laid out for the infrastructure sector, very little ground has been covered when it comes to providing education to our children. While universal access to education has been mostly achieved, the concern about the quality of education is very much valid. The Annual Status of Education Report (2016) highlights several of these loopholes. It brings to light how the proportion of children in fifth grade, who can read a book of second standard, has declined to 47.8% in 2016 from 48.1% in 2014, amongst several other mostly depressing statistics.

Similarly, despite a renewed vigour to improve on our medical infrastructure, our healthcare system remains in a deplorable state. Ayushman Bharat, a mega-healthcare insurance system on the lines of America’s famed ‘Obamacare’, was driven to the hush primarily because despite having established government hospitals all over India, the quality of services rendered in such hospitals were nowhere in comparison to those doled out by speciality private sector medical institutions. Positive mends are being made only of late, with induction of more seats in medical colleges for doctors an encouraging move.

For India to establish itself as a world leader in sustainable growth, it must start investing heavily to promote its research and development institutions. India’s current spending in R&D, as a proportion of its GDP, is a meagre 0.85%. Most advanced economies have ensured R&D spending as high as 4% (South Korea spends around 4.3% of its GDP on R&D operations per year). The recent move to expand the scope of CSR into funding academic studies is very much commendable. Thus, to facilitate the jump from the hoard of assembler economies to the exclusive bandwagon of knowledge economies, quality education must be made a priority sector to focus on. The irony about investing in education is that the effects are not immediately realized; but when they are, they have the potent to shape a ride to fortunes.

The benefits of such heavy investment may present themselves as unwarranted expenditures to the right-wing, but it is to be remembered that a nation can only go as far as its people can. It is thereby without doubt, in the greater interests to sanction funds that help solidify the dream of a secure future, not only for us- but also for generations ahead.

Finance Minister Nirmala Sitharaman’s decision to push for the merger of ten of India’s largest public sector banking units into just four, is both a news to cheer about and a cause of worry. The good news lies in the fact that the efforts are being made to contain the structural rot which had set in across the tardy-moving governmental lines of yore. The bad news is however, quite unsavoury: unless the mega-merger achieves the objectives of cost synergy and finds the middle ground on staff rationalisation, Indian banking’s mega-merger may turn out to be yet another incident comparable to the rather infamous demonetisation phase, without any fruitful gain.

Sitharaman’s view that merging several smaller banks into larger entities stems from the belief that such a move would lead to greater credit-lending capacity and reduce operational costs of lending. This would help create ‘banks-of-scale’, which can leverage a behemoth balance sheet size to serve the needs of an aspiring $5-trillion economy by 2025. The largest of the proposed mergers is the PNB-United Bank-Oriental Bank of Commerce. The amalgamation of Indian banking’s veteran triad would expectedly lead to a net business worth of ₹18 lakh crore, and would thereby right away become the second largest banking network (after the State Bank) in India with a total of 11,437 branches. Canara and Syndicate Bank, once integrated, will render it as the fourth-largest network in India with a potential to cut operational costs heavily due to network overlapping. The last of the mergers, that of the Union Bank of India with the Andhra and Corporation Bank, would enable the coalesced firm to increase the post-merger bank business by a basal factor of two at the very least.

The idea to consolidate the collapsing public sector banking system, plagued by overwhelmingly crippling amounts of NPAs and further accentuated by a lackadaisical staff culture, is not new. The Narasimham Committee in 1990 had recommended a vision similar to that shared by the government to prop up credit-availability and boost the otherwise flailing sector. The Committee had also recommended that it would be prudent to shut down weak banks instead of merging them with stronger ones; but this has never been a politically viable option for any government at the Centre.

Some may argue about the FM’s timing with respect to the sudden need for the introduction of the bank merger proposals. While the government has been a painting a glossy portrait of the economy by cherry-picking data, all is clearly not well. Economic parameters have been telling an alternative story from the government’s propaganda of an economic blossom, revealing the pitiable state that the Indian economy has got itself into. The government’s own admission that the growth in GDP for the first quarter of 2019 has come down to 5%, the lowest in a span of eight years, is only pointer to the riddle at large. The stagnation had set in from last year, with a vicious cycle of falling private investments and job cuts threatening to eat away the precious balance in the delicately organised and inter-dependent sectors. When the investments falls over a consistent period, along with a decline in job growth and opportunities, private players tend to take decisions that remain mostly under the hood. Foreign investors, on whom surcharges were placed shortly after the introduction of the Union Budget, had drawn out their funds in droves, sparking concerns of an impeding recession-like scenario. The worst-hit of these sectors was clearly the automotive sector, which has seen a 35% downfall in sales for July 2019 compared to the same period last year, in consonance with an estimated job loss of around 2.30 lakh positions, data released by the Society of Indian Automobile Manufacturers (SIAM) cautions.

In times of such a deluge, it is often best to hunt down the root of the problem at large. The twin balance sheet problem, in which both the industry and the banks are in the red, can be eliminated by a merger of banks alone, along with government’s capital infusion programmes. The drive comes at a time when the government has received a bonanza from the RBI in the form of a dividend transfer worth ₹1.76 lakh crores- out of which the government has promised a upfront capital infusion of ₹70,000 crores into banks to improve their lending positions already. In a slew of reforms that were announced a week back, the government has also been exploring the possibility of fast-tracking loan applications from Micro, Small and Medium Enterprises (MSMEs) by taking advantage of the liquidity with the PSBs with the last-mile connectivity of the non-banking financial corporations (NBFCs).

While it is clear that the mergers were much required and quite clearly the need of the hour, the question of whether the government would be able to contain the ramifications of the fallout of the simultaneous mergers, each of panoramic proportions, remains unanswered. Consolidation of the ten banks into four is certain to upset industry parameters, but the uncertainty can be contained by putting buffers in place wherever essential. In a bid to mop up the banking sector, the government should also look at the hard choice of terminating the service of under-performing employees over phases to help reduce operational costs in the long run. This may prove politically costly, but such a hard decision would also ensure the due efficiency of the lenders. For now, however, the FM has ruled out job losses due to the proposed mergers. The biggest hurdle is however something that is entirely the ballgame of the government: managerial boards. It would be in the country’s (and the government’s, of course) interests to put in people with a repertoire of financial knowledge and banking experience to lead the consortium of merged mega-banks. After all, dummies can lead well in times of profligacy, but such political compromises only results in diffused accountability when in crisis; and the government has only learnt of it the hard way.

India’s annual budget for the FY2019-20 was presented on the 5th of July by the first woman Finance Minister of India, Nirmala Sitharaman. She aimed to make a sweeping change across a range of sectors, and introduced several measures and methods to contain India’s deficits and maximize growth and output. Amidst a host of other ventures that she (and the government) envisages over the course of the next decade, the numero uno spot is occupied by the dream to scale up India’s physical and social infrastructure. While the latter has had considerable success in the form of an affirmative social sector framework, the former has been found lagging.

The FM introduced a brand of new schemes that will pump in fresh life to India’s wailing infrastructure development story, to the tune of approximately $300 billion dollars a year. A great amount of work needed to be done to bridge the rural-urban gap, and physical connectivity was an essential cogwheel attainment of the objective. The Pradhan Mantri Gram Sadak Yojana (PMGSY), with an ambitious target set to cover 125,000 kms worth of rural roads in the country, has had a budgetary allocation worth Rs ₹80,250 crores and is presently in its third phase. In earlier phases, 30,000 kilometres of new roads in rural areas were constructed, and the construction in all such phases were through applications of green technology. The Highways department was infused with a remarkable ₹83,016 crores for the present fiscal year, its highest ever. The increased spending however, is not misdirected. The Railways, which serves as the lifeline of the nation, was also accorded the limelight, with FM Sitharaman promising to ramp up investment in the Railways to ₹50 lakh crores before 2030. State investment in infrastructure in the long run is almost always beneficial to the economy. Several studies over the course of decades have corroborated the fact.

In India, with private investments falling and several economic indicators in the red, an impetus to the otherwise neglected infra sector will help bring about a transform in the economy. The development of this sector will have an instantaneous cascading effect on other ancillary sectors, and help propel a bullish trend to look out for. Projects such as the UDAN scheme, or the dedicated freight corridor, industrial corridors, Bharatmala and Sagarmala were touted as key highlights with respect to the renewed thrust on such a spending. The government also intends to exploit the riverine advantage unique to India; cargo transporation through the Ganga is set to expand four-fold in volume. The creation of transport hubs will be initiated at Varanasi, Sahibganj and Haldia. This will amplify inter-State trade volumes and help de-congest the arterial highway networks that are overly burdened.

FISCAL INTERPRETATION:

While budgetary announcements are easier said on paper, implementation makes the real difference. The fiscal interpretation to deliver on such high power promises rests on how and when the projects are to be financed. The Economic Survey estimates that an investment of the order of $4.5 trillion over the course of the next twenty-five years would put India in a phase of robust growth and development.

The government is in urgent need of heavy private investments in the infra sector if it is to achieve its agenda. Yet, with structural difficulties embedded in every nook and corner of the legal corridor, and with a generally negative investor sentiment, getting such a high quantum of investments is an uncertainty in itself. The IL&FS’s ₹91,000 crore debt botch-up, an ongoing liquidity crisis in the NBFC sector, and the bank’s NPA woes have only marched ahead to compound the problem.

Sitharaman’s primary thrust was to ease the liquidity crisis that the NBFCs find themselves embroiled in, which would consequently go a long way to provide relief to the strained banking system. While bank credit had increased in the past fiscal year, the credit obtained from banks fell considerably from ₹9.64 lakh crore in March 2016 to ₹8.90 lakh crore in March 2018. The government has devised a panorama of ways to come up with the numbers required for the behemoth capital funding that the infrastructure sector urgently requires. One of the key takeaways from the budget speech was the proposed establishment of the Credit Guarantee Enhancement Corporation (CGER), which would act as an interface for borrowers with assurances and guarantees of repayment to the lenders, and at the same time provide the borrowers with lowered interest rates. The vision to deepen the market for long term bonds, including that for corporate bond repos, credit default swaps, and the like, were extensively discussed. In a watershed moment, the government also permitted investments made by the Foreign Institutional Investors (FII) and the Foreign Portfolio Investments (FPIs) in debt securities, that has to be sold or transferred to domestic investors within a fixed lock-in period.

ON THE ROAD TOWARDS PPP:

In consonance with PM Modi’s dream to turn India into a $5 trillion economy, FM Nirmala Sitharaman divulged investment figures required to take India up the ladder. That is when she highlighted that India’s investments would have to scale up to ₹20 lakh crores a year ($300 billion). The Railway Budget alone would have the lion’s share, clawing into a sizeable ₹50 lakh crores for infrastructural upgrades and system designs between 2018 and 2030.

The FM put forward the idea of modelling the investments on a Public-Private Parnership (PPP) structure. This would, in the eyes of the government, reduce bureaucratic delays, maximize profit, and turn ailing ventures into lively setups that focused on long run benefits and outputs. She proposed to unveil a blueprint for completion and fast-tracking of several projects under the PPP model for works under the NHAI, gas grids, waterways, regional airports and more.

Despite such bullish trends, all that glitters is not gold. Several analysts feel that if the government does not take concrete steps to implement changes in the PPP model on the lines of the Kelkar Committee, the dream to attract investments worth ₹20 lakh crore would only be a dream. Arun Jaitley, a lawyer by profession and the former Finance Minister of India, lamented the fact that despite India being the largest market for PPPs with almost 900 projects, PPP contracts were riddled with “rigidities”, and the failure to develop quick grievance redressal systems plagued their effectiveness. For 2019-20, the PPP component of the extra budgetary resources (EBR) is projected to be 33%. The share of PPP in railways’ EBR in 2016-17 was 51%. Clearly, share of private investors in India’s infra sector is on the decline. A report by rating agency Icra Ltd paints the dismal picture of NHAI, whose debt has risen from ₹25,000 crores in 2014-15 to ₹1.7 lakh crores in 2018-19. The primary cause of the unbelievable rise in debt can be attributed to the linear focus on entirely publicly funded engineering, procurement and construction (EPC) projects.

THE WAY FORWARD:

The Kelkar Committee made a smorgasbord of recommendations that were aimed at simplifying the PPP model, and actually encouraged private players to take interest in State-sponsored projects. Certain recommendations were striking. Model PPP agreements need to be re-drafted to ensure an optimal share of risk-taking among all stakeholders and full disclosure of associated benefits and revised costs must be prominently included. It also proposed to set up independent regulators that are going in for PPPs. It also established four mechanisms to combat operational losses suffered by private players when the project timespan extends for around 20-30 years. In a nutshell, the Kelkar Committee Report on PPP was pro-private investment, and its timely acceptance and implementation can help smoothen out the rough edges of policy-making in this regard.

All in all, unless the government hits the right note and builds an air of confidence in the infrastructure sector, India’s $5 trillion dream would be very difficult to take off. The drive to open the floodgates for increased expenditure on infra investments will pay off in the long run, when the benefits become quantifiable and more visible. It is important that stress is laid on reforming the PPP model, and direct hordes of investments to the infra sector. This would also have parallel benefits, as it would push employment statistics up and support ancillary industries in the process. Tentative benefits are all around, but when do we catch the train to sustainable long run growth?

The annual Union Budget is a subject of unique importance in the working of any parliamentary democracy such as India’s. The Budget, with one sweep, has the potential to churn out a stronger economy, and yet on the other hand, an ability to carve out a bearish effect on the markets. 2019’s interim budget was a departure from tradition in more ways than one; the general principle that an interim budget must not bring about macroeconomic instability was thrown up for a toss. The interim budget drew widespread condemnation for pushing populism over fiscal prudence. This time, however, Nirmala Sitaraman did not leave gaping voids, and played a spectrum of cards that could potentially have long-term ramifications on the economy as a whole.

The 2019 budget presents many positives to take away, which would over time simplify and streamline operations. The government’s pet project, Aadhaar, was in particular highlight. Sitaraman’s maiden budget proposed to make the Aadhar and PAN interchangeable when it comes to filing tax returns. As such, those who do not have access to a PAN card can quote the Aadhaar number wherever deemed necessary. Furthermore, NRIs who arrive in India will from henceforth be issued an Aadhaar card without the existing mandatory waiting frame of 180 days. This would both reduce the bureaucratic hurdle and provide Aadhar-linked benefits to the NRIs without a rather long cooling period. Yet, in its drive to push the Aadhaar as a proponent of unity, the government must ensure that all deserving citizens are provided with an Aadhaar card, and not ostracized from public records. At present, several inconsistencies with the Aadhaar have been earmarked. The administration would do well to lend a ear to the concerns and fix the issues as early as possible.

A focus on a greener India was also on the government’s mind, as it proposed to slash the higher taxation slab of 12% on Electric Vehicles to the base 5%. Sitaraman claimed that the government had moved the GST council to put into effect the change as was mandated above. In consonance with the decision, it was also announced that tax rebates upto ₹1.5 lakh would be awarded for interest paid on loans to buy the electrically-operated vehicles. The move is commendable as it puts India at a head-start when it comes to ensuring cleaner mobility. However, it will not solve India’s auto-sector woes. Neither does it seem pragmatic to throw in bonanzas when the average cost of an electric vehicle is beyond the means of the Indian middle class, which for long has been burdened. India, like the European Union, has decided to not put a compulsory cap on manufacturers to dole out a percentage of their products in the electric vehicles sector. The decision to provide a sudden impetus to electric vehicles proved to be a jolt for many leading analysts and businessmen, who had expected sops elsewhere.

When it comes to the banking sector, there were several eye-grabbing headlines that poured in throughout the day. The government announced a ₹70,000 crore capital fund to replenish public sector banks. This was done to boost credit availability in the midst of an ongoing liquidity crisis. Non-Banking Financial Companies (NBFCs), which were in a difficult spot, in essence got a breather from the budget. The government agreed to provide a partial guarantee to all the State banks for the acquisition of ₹1 trillion worth of highly-rated assets from NBFCs. A revival in the fortunes of NBFCs would cascade into higher credit facilities for the MSME sector, ultimately equating to a stronger output and growth potentialities. Additionally, Sitaraman hailed the Insolvency and Bankruptcy Code (IBC 2016), the promulgation of which had led to the recovery of over ₹4 lakh crore worth of bad loans over the course of the preceding four years. Yet, the issue of a ₹70,000 crore dividend brought up passionate sentiments of the issue of the RBI’s independence as a central bank, which might possibly be under threat for the first time in decades.

The Modi 2.0 government fulfilled its electoral emphasis on the social sector, with capital outflows in other sectors not hampering the grants alloted for the sector. The total expenditure on Centrally-sponsored social sector schemes was pegged at ₹3.31 trillion. A marginal increase in allocations on all fronts were observed in comparison to the interim budget that was presented earlier this year. Subsidies in LPG cylinders and houses for the poor were retained. Under the Pradhan Mantri Awas Yojana (PMAY), spending on rural housing has been valued at ₹25,853 crores. Pradhan Mantri Gram Sadak Yojana (PMGSY), which was a feature mention in Sitaraman’s speech, was alloted ₹19,000 crores for the purpose of establishing rural connectivity through a better road network. Pradhan Mantri Shram Yogi Mandhan Yojana, a new scheme that was shown the red carpet in the interim budget, would now cover 30 lakh workers, each of whom are eligible to receive ₹3,000 as a monthly pension after they turn sixty.

The 2019 Budget also drew a fair share of flak and criticism for a wide number of reasons. Start-ups and investors, however, were left a tad bit disappointed. The speech declared that “… start-ups and their investors who file requisite declarations and provide information in their returns will not be subjected to any kind of scrutiny in respect of valuations of share premiums”. The Budget mentioned that a mechanism of ‘e-verification’ would be put in place to establish the identity of the investors and the source of their funds, without providing an approximate timeline for its rollout and implementation. This provided little clarity and was ambiguous, at best. Furthermore, in what could possibly signal bureaucratic interference, the government spoke of a ‘special administrative arrangement’ for prompt redressal of grievances and pending assessments of newfangled firms.

When it came to corporate tax, the government said that companies with an annual turnover of ₹400 crore or less would now fall under the 25% tax slab, as compared to the ₹250 crore cap earlier. Many critics slammed the government for providing reliefs to a specific pie in the industry rather than bringing about significant changes in the tax structure for the corporate world. For a government that relies on hyper-nationalistic sentiments and openly flaunts jingoistic tendencies, no specific mention of the Defence sector was indeed a surprise. Also, when the job distress is at its peak (CMIE, December 2018 report), there were no specific measures that were adopted by the present dispensation to ease the aching pain that jobseekers across the country felt. In what could generate a lot of political friction, additional levies were planted on diesel and petrol supply to the tune of ₹1 per litre. Most interesting of all, however, was the government’s “expectation” of a higher dividend payout from the RBI- bringing back the thorny topic on the autonomy and independence of the RBI into the forefront.

The annual budget that was presented on the 5th of July seemed more expedient when it comes to governmental spending and providing sops. However, contentious issues and fears were not allayed by the government, thus evoking several questions. The fiscal deficit target was set at 3.3%, and the government has stated fiscal consolidation as one of its primary agendas that it seeks to pursue. The deficit margin is in close proximity to the NK Singh Committee’s recommendations on the FRBM Act, 2003, which proposed a fiscal deficit of 3% till 2020. In all probability, though, the deficit will exceed 3.3%, and it will be an extremely hard job for the men in North Block and beyond to contain the deficit at the proposed figure. The 2019 budget, which was expected to be a high-octane event, was rather meek by its standards. Amidst the fanfare of the cricketing season, perhaps Anand Mahindra adeptly summarised it when he remarked that all that Nirmala Sitaraman took was ‘steady singles’, when all were looking forward for the ball to be hit out of the park!

West Bengal has had for long a volatile political history. With several instances of mass-scale rebellions and violent uprisings against the administration throughout expansive swathes of time, the state has certainly enough potent to be labeled tempestuous. After a spate of gross misuse of power and unabated killings (Sainbari murders, Marichjhapi massacres, Nandigram) for a period of thirty-four years, Mamata ascended to the center-stage of West Bengal politics as the Chief Minister in 2011. Her party, the Trinamool Congress, had ridden to power through the catchphrase, ‘Maa Mati Manush’– promising people development (‘unnayan‘), and an immediate end to administrative high-handedness.

Almost eight years later, the ground reality looks immensely far-fetched from the poll planks of 2011, and murders have once again reclaimed their spot as a political weapon.

Venomous Roots

Mamata has always been a mile away from the bhadralok-zamindar politics of the state; her repute as a militant street-fighter battling for the oppressed and destitute propelled her popularity among the masses. After assuming office, it only metamorphosed into a brand of politics that encapsulated populism, outreach efforts, and loyalty-garnering initiatives. There is no denying that in terms of social ventures, Banerjee has outdone most other politicians of her era; providing opportunities for the girl child (Kanyashree), and offering artisans, craftsman, and folk singers appreciable remunerations for their services. These activities have helped generate an army of party loyalists- being the beneficiaries to the government’s social schemes, these men had a call of obligation. Her party’s base continued to grow naturally until it hit the saturation point. And that is precisely when the trouble started.

With growing support and politicisation of the bureaucracy (much like her Communist predecessors), complacency had begun to sow its seeds among the party ranks. Thus, when the base growth stalled and became evident, workers tried to brute force their way to gain the vote of those in ideological contrast to that of the TMC. Fiery leaders like Anubrata Mondal, TMC’s Birbhum district president, flaunted veiled threats as tools of intimidation. Infighting had already commenced, thus eroding away the electorate’s confidence in the ruling disposition. Brazen remarks made by several high-ranking party members (read, Tapas Pal) had left little to prove that the party functioning was completely arbitrary.

Political greed, coupled with the onset of deplorable complacency, also opened the floodgates for corruption. The Narada sting operation revealed how 11 of her ministers accepted bribes in exchange of unofficial favors for a fake consultancy firm floated by the whistleblower himself. The Saradha scam mired her repute as a leader who takes on corruption- and suicide figures for those who lost all in the ponzi scam reached double digits. Despite such brutal revelations, she miserably failed to take any definite action against the accused, and went on to harbour such men in order to extract political reaps owing to their unprecedented influence.

Appeasement Politics and Support Banks

Prior to Independence, the Muslim population in Bengal was estimated at 29.5%. Post partition, however, that figure dropped to 19.85%. However, after the 1971 Indo-Pakistan war and establishment of Bangladesh (formerly East Pakistan), the percentage again ricocheted to 20.46%. When Banerjee came to don the hat as a Chief Minister, the demographics resembled a 27% share of the Muslim population, and a 70% share of the majority Hindus.

Sensing an opportunity to lap up the Muslim vote (an electorally significant 27%), the TMC supremo went all guns blazing to provide Muslims with benefits unparalleled. Her brand of appeasement politics is nowhere near subtle; her extravaganza in terms of playing the religion card is downright offensive. Calcuttans have got used to the sight of Mamata draped in a white scarf over her head offering namaz prayers during prominent Muslim festivities. The Dinajpur-Maldah-Murshidabad-Birbhum region has seen specific religion targeted efforts to win over the vote bank. However, such concerted effort towards minority appeasement has weaned off many. In 2016, Firhad Hakim, one of Mamata’s many trusted lieutenants, reportedly described Garden Reach as “mini-Pakistan”. A feature report by THG highlights how in the Falta block of South 24 Parganas, the alleged ‘monstrosity’ of TMC leader Zahangir Khan has accentuated the TMC’s rootless politics. This year, she increased the Eid bonus for all Muslim State employees to Rs. 4000, a 11% hike from last year.

Mamata has one trick up her sleeve that yields her big results: fielding celebrities! It seems to serve two objectives at once: while the stars bring along their own fan following to the advantage of the party, it also helps push party factionalism under the carpet. To take on the BJP’s Asansol candidate, Babul Supriyo, Banerjee placed yesteryear actress Moon Moon Sen as a contestant for the seat. Nusrat Jahan and Mimi Chakraborty, two eminent actresses from Bengal’s film industry, also found a place amongst the 42 prospective MP candidates, contesting the elections from Basirhat and Jadavpur, respectively. Tollywood star Dev Adhikari, one of the industry’s leading figures today (how pathetic!) is also in the fray this time around, from Ghatal. While the strategy is a complete winner in the short term, applying band-aid fixes to rifts within the party ultimately produces defectors, or worse, moles.

For residents of Kolkata and its suburban areas, the anarchy of auto-wallahs is beyond grasp. The auto drivers and toto (e-rickshaw) operators have pacts with local leaders in exchange of uninterrupted ‘do-what-you-may’ regime. Cases of road rage against such people are shelved by the police; in short, their supremacy on the roads remain unchallenged under the patronage of their political masters. Hawker encroachment, also allegedly under the patronage of local leaders, has rendered the wide majority of pavements inaccessible to pedestrians, exposing them to the perils of walking on busy roads at peak hours. These pacts are nothing but purely based out of monetary and vote considerations. As police action is de-facto forbidden, they continue their reign of pandemonium unfettered- and drop the votes alongside.

Industry Aversion and Syndicate Raj

Banerjee’s breakthrough moment in Bengal’s tense political environment was when she single-handedly spearheaded a campaign to drive out the TATA Group from Singur, alleging forced encroachment of farmer’s lands by the CPI(M) government. Her relentless protest ultimately ensured that the Nano project withdrew from Singur, marking a thumping win for her against adversities. Co-incidentally, as fate would have it, a marked decline in industrialization has been the jinx in her term as the Chief Minister.

In her first stint (2011-2016), the contribution of industry in West Bengal’s GSDP shrank from 19.1% in 2012 to 18.8% in 2013. Manufacturing also witnessed a progressive decline from 56% in 2012 to 55.3% in 2013. A report by the Business Standard in 2013 also highlighted a 97% decline in industries since 2010, and an 85% fall when compared to 2011. Since then, efforts were made to salvage Bengal’s flailing economy. The Global Bengal Summit was conceptualized in 2014 and has since been instrumental in attracting investment proposals into the state. In fact, in 2019 itself, the 5th Global Bengal Summit generated investment proposals worth Rs. 2.84 trillion. However, when it comes to implementation, the statistics are no longer rosy as they were on paper: growth and industry expansion is happening at an extremely tardy pace. Bengal has also squandered the opportunity of riding the demographic dividend, i.e. to cash in on the productivity of the working age population, a report from the UNFPA suggests.

The problem is multi-pronged and poses as a conundrum to the political dispensation. If the INTTUC (the party’s trade union arm) is to be strengthened, it will help bolster party recruits and drive support for the party. However, a strong trade union would also ride roughshod over the managerial decisions, and any complications would keep further investor interest at bay. So far, the Trinamool Congress has not been able to find a viable solution to this stumbling block on the road to development.

The Kolkata flyover collapse, allegedly linked to the Syndicate providing inferior-grade materials for the construction

In cities, however, the problem assumes a radically different dynamic. Construction land, building materials, and sand are all controlled by a group of people who remain politically affiliated to the ruling party- termed as syndicates. Extortionism is common, and any buyer who seeks legitimate means of transactions would be compelled to ‘give in, or give up’. Often, these syndicates provide an inferior quality of construction materials at a higher price, widening their pockets with profits. This has inadvertent effects. Repair work done by the State’s Public Works Department turns out to be temporary and inadequate. In 2016, a flyover collapsed over Girish Park- a crowded locality in Kolkata, with later inspections revealing the supply of inferior-grade materials as one of the chief reasons for structural instability.

Rise of the Right Wing

Amidst an atmosphere of uncertainty, the biggest gainer has undoubtedly been the Bharatiya Janata Party. Drawing from its proven formula of polarisation of voters along religious lines, the party primarily projected itself as a binary alternative to Mamata’s Muslim-first policies. It had all the positives in the world to begin its journey with:

The party effectively relied on Modi’s mass appeal, particularly among the youth of the state- promising ‘sabkasaath, sabkavikaas‘ (inclusive development for all).

The Left, which was completely routed in the 2019 Lok Sabha elections, had its entire vote base transferred to the BJP, and,

The theme of national security and an unprecedented influx of illegal Bangladeshi immigrants into Bengal were repeatedly underscored to rake up jingoistic sentiments.

The Bharatiya Janata Party, which had no significance in Bengal’s poll map, has made a surprising wildcard entry to play an integral role in the complex workings of the State’s politics. It will be interesting to observe how the right-wing, which focuses on the base of Hindutva, fares in a state where Muslims form a significant chunk of the population. Furthermore, the electorate expects the BJP to make the paradigm shift and ensure policy changes, to facilitate rapid industrialization of the state. While Modi’s Gujarat model is easy to sell as an ideal model, Bengal is not Gujarat: the state arm of the BJP will face tough challenges in its quest for acche din.

The Way Forward

Bengal’s explosive mix of greedy politics, minority appeasement and populism is certainly a disaster waiting to happen. Political violence is on the consistent rise. The Panchayat polls in 2018 were one of the bloodiest in Bengal’s history, with 25 people being slain as part of political rivalry. Post-poll violence after the 2019 Lok Sabha elections is so bad that an imposition of President’s Rule is being pondered over as an option to tackle the absolute lawlessness that Bengal is reeling from today.

The fantastic irony lies in the fact that a leader who comes from a background of fighting against heavy-handed establishments, has herself succumbed to the vagaries of electoral rapacity! Under Mamata’s regime, ‘red fascism’ of the Left has merely been replaced by secular fascism, and the Trinamool Congress is essentially old wine served in a new bottle.

To begin with, Mamata must have a hard look at her own policies- often crafted with vested interests- and alter them at the earliest. Second, she must look to fill bureaucracy with competent officers, and not puppets: it will ensure that she gets sound advice on critical issues pertaining to efficient governance. Third, she must reign in lumpen elements operating from within the party, as a party with leaders who are mutually out of sync damages both the party as well as good governance. Fourth, she must make a dedicated effort to stop the syndicate raj and illegal sand mining that rot the State machinery, as her silence only fuels such activities. While her party stands to lose significant amounts of donation amounts coming from such illegal syndicates, she would be free of the moral guilt, and more importantly, the taint of giving a free hand to such elements. Fifth, and most importantly, it is time that she introspects the demographic damage that minority appeasement is doing to West Bengal’s cultural lineage. State security, as well as an irreparable cultural heritage, should never be toyed with in a bid to polish vote banks.

At this hour of desperation, Mamata needs not only an image makeover but also an administrative rejig, to make things work for the TMC. I can only keep fingers crossed, and hope that sense prevails soon. It would be apt to recall Ellen Glasgow, the famed American novelist, who had prognosticated that “… all change is not growth, as all movement is not forward.” If only the Trinamool Congress could draw some lessons.

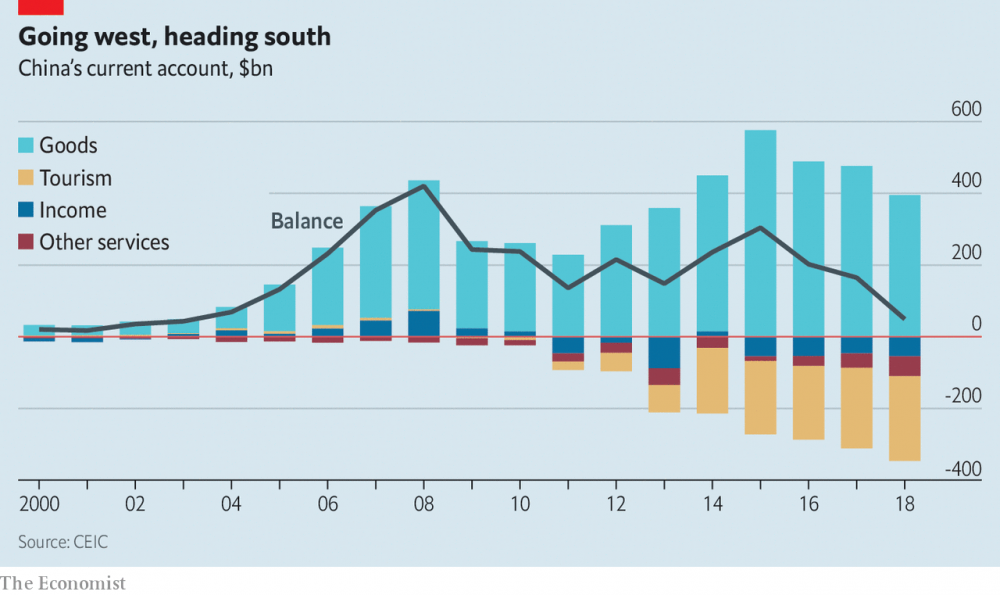

The fact that China has been a vociferous exporter and a tame importer of global goods may not come as much of a surprise. What hits hard, however, are the numbers behind the game. That ratio, disproportionately behemoth, was pegged at 127.16 (December 2018): which is to say, Chinese exports was a mind-boggling 127 times higher than its net import! All through these years, as an almost direct consequence, China has had an current account surplus. The time for merry-making may soon be running out; as China today faces the threat of racking up a current-account deficit for the first time in decades.

Analysts at global agency Morgan Stanley predicts China may face an imminent deficit in 2019, the first time since the last such deficit arose in 1993. This metamorphosis from a state of surplus, to that of a deficit, will bear an immediate cascading effect on both the Chinese economy, as well as State-run institutions. The Chinese model under Xi Jinping has become increasingly closed-door, with several accusations of skewed policy priorities for local competitors and expropriation of foreign-based technology. This shift might represent a rare willingness to jump over onto an era of economic liberalization, a perennially sore point between the interests of the United States and its Chinese counterpart.

Looking at the roots

Historical economic data makes it clear that China has saved way more than it invested. However, the working progeny of the yesteryear generation has almost an imbued tendency to splurge more. This is made clear by exponential increase in the consumption of smartphones, cars, and other luxuries. A report published by CEIC Data highlighted how Chinese tourists were the largest spenders abroad. In 2018 alone, China ran a $240 billion deficit in its tourism industry- its highest yet. This problem is only set to aggravate, as an ageing population draws down its savings, thereby further complicating matters.

A deficit in the year ahead will be negligibly small with respect to the Chinese GDP. Moreover, China has a sizeably good buffer of $3 trillion worth of foreign exchanges that could be used to head down immediate triggers of worries. This should give China time. What remains to be seen is what China does to revive its flailing mast. In April 2019, China is set to enter the Bloomberg Barclays bond index, which would help accelerate foreign funding into Chinese bonds to the tune of approximately a hundred billion dollars, all within two years. It has also eased quotas for foreigners who buy bonds, apart from luring pension and mutual funds who would now think about increasing their exposure to China.

Yet, on the reform front, moves remain limited. Restrictions for Chinese citizens were enforced in late 2017 on monetary withdrawal from Chinese banks overseas- and was capped at $15,000. While the official statement read that it was aimed at curtailing terrorism financing, money laundering and tax evasion, the fine print is not difficult to read this time around. China clearly has a sense of the upcoming perplexity. Such hardline State control may ultimately deter external investors from pumping their money into China, as it is uncertain if money once pushed in, can be taken out with ease. A system which treats locals on a higher ground than foreigners is not only conceptually flawed, but also smacks of corruption and instability.

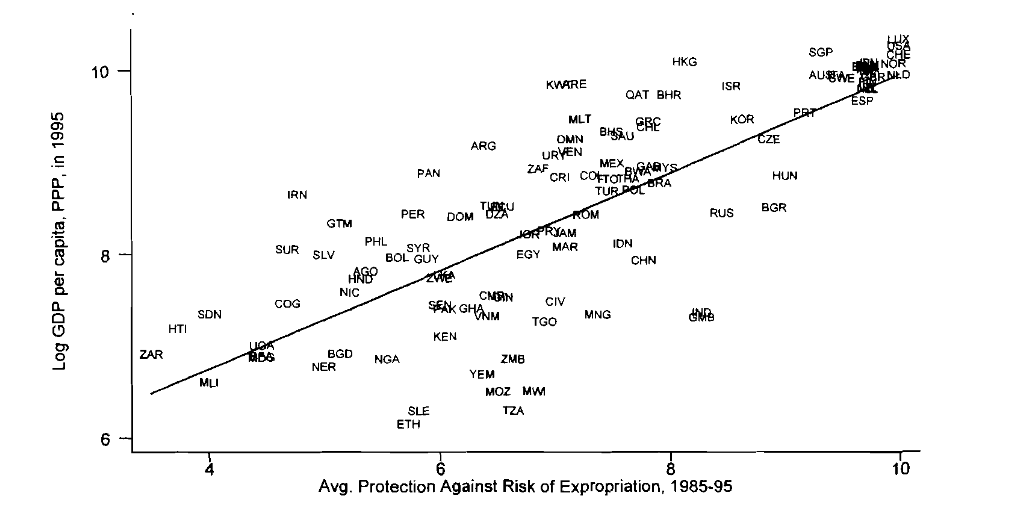

Economists Douglas North, Daron Acemoglu and James Robinson have in a paper shown that the development of an open political system, aided by strong state institutions, help foster long run growth. While the West would inevitably want China to return to normalcy and develop institutions of global credibility, any such turn under Xi’s rule was out of question. In January, China reported that its economic growth cooled down to its lowest in twenty-eight years. This development is in line with the steep fall in exports, which fell an unexpected 4.4% in December 2018, along with a contraction in manufacturing activities.

Figure 2: A Graphical Representation of North, Robinson and Acemoglu’s work of a linear relationship between openness of institutions and long run growth.

Acute Debt Problem

On top of that, exists China’s humongous debt problem. China’s pile of $34 trillion dollar worth of public and private debt is akin to a ticking “debt bomb” to several economists. Among the forefront of such vocal critics is Arvind Subramanian, who brought out two pivotal pieces in Project Syndicate last year. Subramanian argues that China’s tactic of cooling down financial crises through increased State investment in domestic infrastructure projects only help embroils, or rather disguise, the mess that the debt represents. A near-normal economy that runs with a whopping 270% debt-to-GDP ratio is unarguably beyond the laws of economics. To put a benchmark reference, the Greek economy collapsed when debts reached 188% of the GDP. Stein’s law holds that if something cannot go on forever, it must stop. Yet, Chinese debts are on the roll. It has repeatedly tried to finance its domestic debt through external investment that reaps bountiful profits for China. The Belt and Road (BRI) initiative, that spans 68 countries and involves 40% of the world’s GDP, is one such attempt. Countries, however, are only growing aware of the increasingly compounded terms of such Chinese projects: even workers for those projects are of Chinese origin. Several countries have already cancelled Chinese projects due to high fiscal stress. The newly elected Malaysian Prime Minister Mathir Mohammed cancelled $22 billion worth of Chinese projects, which were passed by his predecessor Najib Razak, as such projects would be an added burden for Malaysia’s promising economic future. China’s loaning system is inherently biased, and to the extent that Harvard University’s Ricardo Hausmann recently termed it usurious.

The Road Ahead

On an overall front, the current fiscal year should be the year for undertaking structural reforms to the Chinese economy, to help it become more resilient against internal volatility and the threat possessed by an ageing workforce. This must be backed by political willpower, as such changes will help ensure benefits in the long run. The US-China trade war is only the fruit of a myopic vision on both ends: while China seems to resist liberalization on the front that it would seem pliable to western ascendancy, America’s continued persistence on the importance of a stable yuan over far greater concerns of a global slowdown as a result of the under-performance of the Chinese economy is upsetting.

It would be wise to recall Rüdiger Dornbusch’s law, which cautions that “[t]he crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.”

The Interim Budget prima facie looks like a blunt attempt to appease important sections and classes in India that could reap rich electoral dividends: with the limelight on the farmer, the salaried taxpayers, and the demographically strong unorganised sector. Departing from the convention that interim budgets must do no macroeconomic harm, it was an instrument to drive votes for the meeting of narrow political ends. This is thus, a textbook case of populism over prudence.

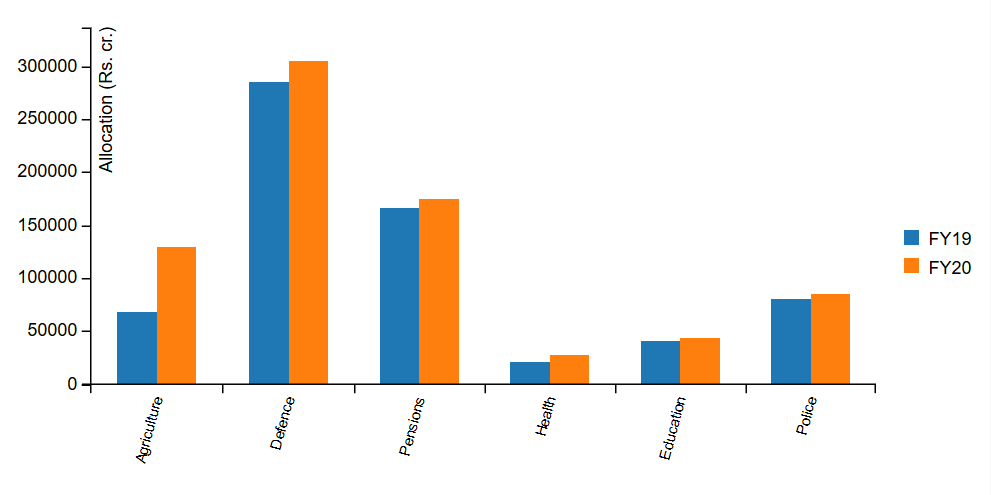

The Union Budget allocation for 2019-20 is about 10% higher than that of its predecessor, with an outlay of ₹27.8 lakh crores. While most sectors witnessed a rise in allocation of funds in absolute terms, their share as a percentage of the total funds demarcated has fallen. Interest payments on debt accounted for the lion’s share in the 2020 budget: 24% (₹575,795 crores). Defence sector spending came a close second (₹284,733 cr), and was followed by subsidies (food, fuel and fertiliser subsidies), which totalled an expenditure of ₹264,336 crores (10-11% each).

Above: Comparison of Funds Alloted to Different Ministries

The budget was expected to primarily focus on a resolution to the agrarian distress, but the government went out of its way to ensure that the middle class and the informal sector workers did not harbour any feeling of being left out. Hence, the budget was mostly an appeasement budget; one laced with doles and sops- and hardly any revenue-generating schemes. Under the Pradhan Mantri Kisan Samman Nidhi (PM-KISAN) scheme, farmers who have holdings less than 2 acres will be entitled to an annual sum of ₹6,000 per family. The agricultural distress is a resultant of traditionally low rates of productivity, coupled with drastic price falls and low size of farm holdings. In an op-ed, C. Rangarajan writes how the average farm size declined from 2.3 hectares in 1970-71 to 1.08 hectares in 2015-16. This is a barrier to efficient use of modern agricultural methods, including mechanisation and other novel technologies like precision farming, which can push current production capacities to a new horizon. Thus, a price support mechanism must be put in place urgently. The government’s hastily announced PM-KISAN, while harbouring good intent, has several fault lines. A permanent solution can only be implemented once long-run considerations are taken into account. Telangana’s Rythu Bandhu scheme which offers ₹10,000 per acre, per year, is more inclusive and is a better choice overall. Odisha’s newly introduced KALIA scheme is also a step in the positive direction.

The Modi government has come up with sufficient relief for the middle class, targeting especially the salaried group, and workers lodged in the informal sector. The Income Tax exemption limit has been raised to ₹500,000 from ₹250,000. This is a direct blow to the already frailty tax collections in India. Income Tax departmental data for the year 2017-18 showed that 66% of the return filers fell under the ₹5-lakh bracket. Hence, the move will wipe out almost 66% of all previously eligible taxpayers from the tax net, and is sure to dent any immediate prospects of tax-fuelled growth. The standard deduction limit has been raised from ₹40,000 to ₹50,000. The Pradhan Mantri Sharam Yogi Maandhan Scheme has been developed as a mega-pension scheme for the unorganised sector, which will pay ₹3,000/- a month to registered beneficiaries. The recent CMIE Report has highlighted how 11 million jobs were lost in 2017-2018 alone, out of which 8.8 million were women.

Union Finance Minister Piyush Goyal announced that in a bid to fund the newly introduced schemes, the government would miss its fiscal deficit target not only for the upcoming year, but also for 2020. Governmental fiscal deficit for 2018-19 and 2019-20 would be 3.4%. In fact, funding the PM-KISAN scheme alone would entail a DBT burden of ₹75,000 crore to the exchequer. The NK Singh Committee on the FRBM Act, had proposed that the fiscal deficit was to be contained within 3.0% of GDP in FY18-20, 2.8% in FY21, 2.6% in FY22, and finally 2.5% in FY23. The government has thus, in the act of fiscal profligacy, sent fiscal prudence for a toss. Furthermore, while the government is overly enthusiastic about a sharp spike in GST collections, the fact remains that receipts from the GST is ₹1 trillion less than the budgetary estimates. Fiscal marksmanship analysis must be implemented rigorously and should try to close the gap between actual and predicted values.Arvind Subramanian mentions that while new schemes are constantly introduced, old schemes that are no longer relevant are hardly taken off the funding radars. This glaring error costs the government by causing fiscal leakage. For example, there is a ninety-six year old scheme, called the ‘Livestock Health and Disease Control’ (under the Department of Animal Husbandry), and it was alloted ₹251 crores in the Union Budget 2015-16. Moreover, pile up of new, expansive schemes pushes the government into higher debt levels. Celebrated Harvard economist Kenneth Rogeff, had predicted that countries with a debt/GDP ratio greater than 90% experience negative growth rates. This was evident through breakdown of Greece’s financial environment. Greece had a staggering debt/GDP ratio of 188% when the economy collapsed. India’s debt/GDP in 2017 touched 71.18% in 2017, and came marginally down to 69.55% in 2018. Thus, consistent and serious efforts must be made to bring down the debt levels.

Global rating agency Moody’s has marked India’s interim budget as “credit-negative”, underscoring the fact that it has only give-aways and little to recover from. Business tycoon Anand Mahindra remarked that the budget was a “pump-priming” exercise for the government, as higher incomes would lead to greater consumption and drive growth. In my opinion, several schemes that have little rational base can be wiped off and their funds can be relocated to more efficient schemes. For example, farmer support which has been pegged at ₹6,000 can be increased if fertiliser subsidies are decreased, as excessive use of fertilisers and soil enhancers takes a toll on the long term farm productivity (we are over-discounting fertilisers in any case). Disregard for fiscal discipline, especially in times when the chilly winds of protectionism are blowing all over the global economy, is a dangerous trend. As Paul Krugman puts it aptly, it is prudent to maintain “profligacy in depression, and austerity in good times”. Well said!